With the end of the financial year fast approaching, now’s the time to get on the front foot with your tax planning. Taking a proactive look at your position before 30 June can help you manage tax liabilities, uncover potential savings, and make informed decisions for both you and your business.

Effective planning starts with understanding your broader personal and business goals, along with your cash flow, so any strategies you implement are both practical and aligned with your objectives.

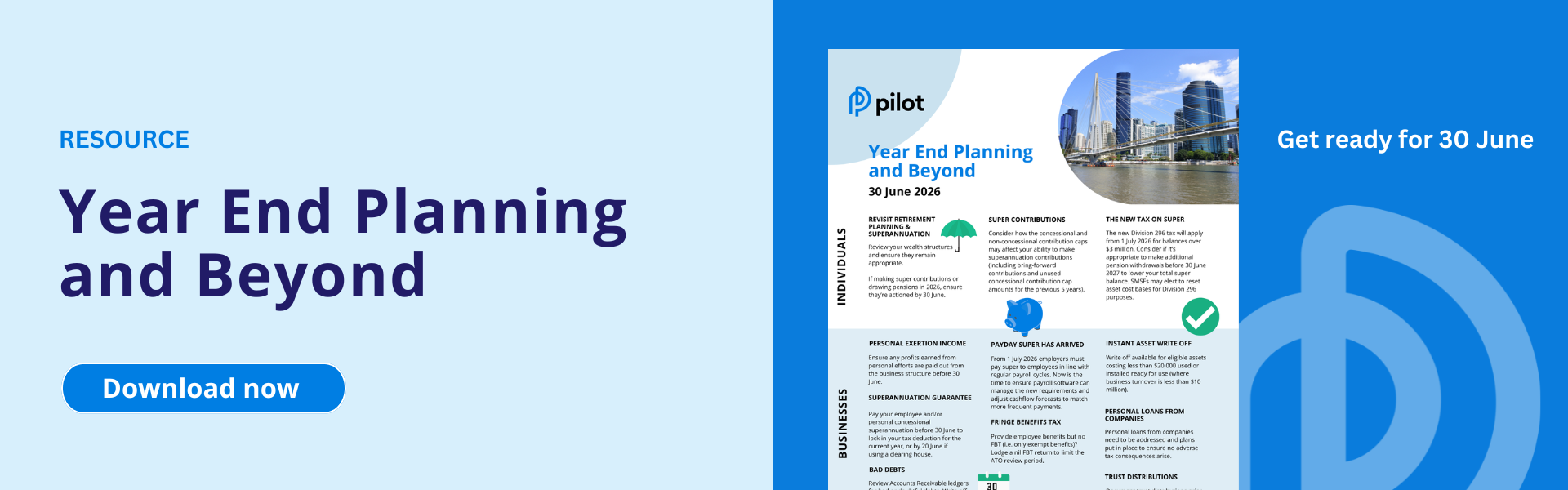

We’ve highlighted the key areas to focus on in our year-end infographic and further details are below.

We have also compiled a detailed list below of the areas to be considered and potentially addressed by individuals and businesses when preparing for 30 June.

Quicklinks

INDIVIDUALS

Revisit Retirement Planning

Review your wealth creation structures, ensure that they remain appropriate and continue to meet your requirements prior to 30 June 2026.

If you have started a pension from superannuation, it is important that you have drawn the required minimum pension for the current financial year before 30 June 2026. The minimum pension payments for the 2026 financial year are based on the member account balance as at 30 June 2025, and are as follows:

| Age of Beneficiary | Percentage Factors % |

| Under 65 | 4 |

| 65-74 | 5 |

| 75-79 | 6 |

| 80-84 | 7 |

| 85-89 | 9 |

| 90-94 | 11 |

| 95 or more | 14 |

There is no maximum limit, except for transition to retirement pensions which is limited to 10%. The payment amount will be calculated based on the member account balance as at 30 June 2025.

The New Division 296 tax on super has arrived

After extensive revisions, the Government’s Division 296 legislation was finalised in March 2026 and comes into effect from 1 July 2026. The legislation introduces additional taxes on earnings related to super balances over $3 million, and again on balances over $10 million. While the initial proposal sought to tax unrealised gains, this is no longer the case.

The additional 15% tax will be applied against any earnings relating to the portion of individuals’ super balances that are between $3 million and $10 million. As this tax is in addition to the standard 15% tax on super earnings, this effectively results in a tax rate of 30%. For individuals with super balances above $10 million, a further tax of 10% applies to any earnings related to the portion of the balance that is above $10 million.

The Division 296 tax applies to taxable super earnings of individuals whose total superannuation balance (TSB) exceeds $3 million. In the first year (being the 2026/2027 financial year), the tax will be applied based on the TSB as at 30 June 2027. For future years, the higher of the TSB on the previous 30 June and year-end TSB will be used.

Super contributions – individuals

Concessional contributions

Individuals are able to make personal concessional contributions from post-tax funds to claim a tax deduction in their income tax returns for the year ended 30 June 2026. The tax deduction is only deductible in the 2026 tax return where the superannuation fund receives the contribution by 30 June 2026. The general concessional contributions cap is $30,000 for the 2026 financial year (increasing to $32,500 from 1 July 2026).

Where you have an unused concessional cap amount from the 2021 through to 2025 financial years, the carry-forward arrangement may be utilised to make extra concessional contributions in the 2026 financial year. This arrangement is available if your total superannuation balance as at 30 June 2025 was less than $500,000 and you have, or are planning to, make concessional contributions in the 2026 year that exceed the general concessional contributions cap.

The additional concessional contributions relate to any unused cap amounts from previous years starting from the 2021 financial year (unused cap amounts from 2020 have now expired). The unused cap is able to be carried-forward and used in a future year, although it expires after five years. Any unused concessional contributions remaining from the 2021 year will expire on 30 June 2026 if not utilised before this date.

When making any additional concessional contributions before 30 June 2026, it is important to:

- Identify your specific contribution cap – is it limited to $30,000 or can you access the carry-forward arrangement?;

- Confirm the amount of superannuation contributions that have been received by your superannuation fund during the financial year; and

- Understand what your employer (if applicable) will still contribute prior to 30 June 2026.

This will assist with ensuring the concessional contributions cap is not exceeded for the period ended 30 June 2026. If a taxpayer exceeds the 2026 cap of $30,000 (and any carry-forward cap), the excess amount is included in their 2026 income tax return and taxed at their marginal tax rate.

Non-concessional contributions

Individuals are able to make non-concessional contributions for the year ended 30 June 2026 where their superannuation balance is less than $2 million at the end of the previous financial year (to increase to $2.1 million from 1 July 2026). These contributions are not tax deductible and are not taxable in the superannuation fund. The non-concessional contributions cap for the 2026 financial year is $120,000 (to increase to $130,000 from 1 July 2026).

If you are under 75 years of age, you may be eligible to make contributions above this annual non-concessional contributions cap by gaining access to future year caps under the bring-forward arrangement. This is reliant on the bring-forward arrangement not being utilised in the previous three years.

The bring-forward arrangement allows you to make extra non-concessional contributions without the requirement of paying extra tax. The availability of this arrangement in this financial year will depend on your age and total superannuation balance as at 30 June 2025. The relevant bring-forward limits for the 2026 financial year are as follows:

| Super balance at 30 June 2025 $ | Maximum non-concessional contribution for the first year $ | Bring-forward period |

| Less than 1.76 million | 360,000 | 3 years |

| 1.76 million to less than 1.88 million | 240,000 | 2 years |

| 1.88 million to less than 2 million | 120,000 | No bring-forward period, general non-concessional contributions cap applies |

| 2 million and over | Nil | N/A |

Individuals with multiple employers – opt out of receiving Super Guarantee (SG) payments

If you are an individual with multiple employers, you may be eligible to opt out of receiving SG from some of your employers (conditions apply). This may help you prevent unintentionally going over the concessional contributions cap and avoid paying extra tax. To opt-out, the ATO must receive the employee’s application for a shortfall exemption certificate a minimum of 30 days before you want the exemption to start.

If you are considering applying for an exemption certificate, discuss this with your employer first. The employer is able to choose to disregard the exemption certificate and continue to pay SG.

Rental properties

For rental property owners, it is important to begin assembling relevant documentation including expenditure receipts to prepare for your 2026 tax return. This includes determining deductible expenses and considering what capital gains tax implications may arise in the event of a sale. The timing of the deductions available may vary for eligible expenses such as rates, property management fees, capital works and depreciation.

Subject to sufficient cash availability, you may consider prepaying interest or paying for other expenditure before 30 June 2026 to crystallise a tax deduction in the 2026 income tax return.

It is also important to review loans and policies to ensure that any interest-only periods are not nearing expiry. Further, consider if any loans have been refinanced for other purposes as a portion of the interest may not be deductible.

A significant shift in 2026 is the ATO’s revised approach to deductions for mixed-use holiday homes. Our earlier article outlines the changes, including disallowed deductions for standard property holding costs (e.g. interest, land tax, repairs). The ATO has indicated their “transitional compliance approach” ends from 1 July 2026 – as such, taxpayers will be expected to comply with the new rules going forward.

Working from home expense deductions

For the 2026 income year, individuals must utilise either the actual costs or the fixed rate method to calculate a deductible working from home amount. The fixed rate method is 70 cents per hour worked from home and covers energy expenses, internet, stationery and computer consumables, without the requirement for a dedicated home office. Additional deductions can be claimed for the decline in value of assets such as computers and office furniture; repairs and maintenance of these assets; and cleaning costs for a dedicated home office.

To claim a working from home expense deduction, you must keep the relevant records. The record requirement is different depending on which method you choose:

- Fixed rate method – taxpayers are required to keep exact records of hours worked for the whole year – a reasonable estimate is not sufficient. The ATO also requires evidence that the taxpayer paid for all expenses covered under the fixed rate method. Further, records for other expenses claimed as a separate deduction must be held.

- Actual costs method – taxpayers are required to keep a record of all hours worked from home for the entire income year or a 4-week representative diary together with evidence of expenses being deducted such as receipts, bills and how the amount was calculated.

The $1,000 instant tax deduction

While the current government has proposed a $1,000 immediate tax deduction for work-related expenses, this change is not yet law. This proposed law is expected to apply to the 2027 financial year and later years.

If legislated, broadly Australian resident taxpayers who derive assessable labour income can claim a $1,000 standard deduction without substantiating expenses. Taxpayers who incur work-related expenses above $1,000 can still claim deductions under the usual rules.

BUSINESSES

Super guarantee – employers

Employer superannuation contributions

Superannuation is deductible when paid. Therefore, to claim superannuation as a tax deduction for the June quarter (or month where the business pays superannuation monthly), the business must ensure that this superannuation is paid before 30 June.

Importantly, if you use a clearing house, you may have to make the superannuation payment to the clearing house by 20 June 2026 to ensure the payment is made to the employees’ funds by 30 June 2026.

Small Business Superannuation Clearing House (SBSCH)

From 1 July 2026, the SBSCH will be closed due to the implementation of Payday Super. If you have not already transitioned from this clearing house, you should be putting steps in place now and commence using a new clearing house before 30 June.

Payday Super is Here

The government’s new Payday Super requirements will begin from 1 July 2026, meaning employers have only a few weeks left to ensure superannuation guarantee (SG) payments are aligned with regular payroll cycles. Under the new regime, SG contributions must be paid and received by the employee’s nominated super fund within seven business days of payday (with only limited exceptions). This is a fundamental change from the current quarterly system.

It is essential that employers ensure their payroll software can handle the new requirements, and that cashflow projections account for regular SG contributions.

To reduce risks of non-compliance post 1 July 2026, we recommend that you act now and are prepared for these changes as soon as possible.

For more information on Payday Super click here.

Personal exertion income

Broadly, personal exertion income is income derived by the personal efforts or skills of an individual. Typical industries where personal exertion income is derived include (but are not limited to) medical professionals, financial professionals, information technology consultants, architects, and engineers.

Where personal exertion income is derived through structures such as trusts, partnerships or companies, the income (less certain deductions) is attributed to the individual who performed the services. It is important to ensure that profits earned from personal efforts when operating via a trust, partnership or company are appropriately paid out to the relevant individuals before 30 June 2026.

This is also an area of our tax law that has received increase focus from the ATO in previous years. Further information on personal exertion income, personal services income and personal services business can be found here.

Allocation of professional profits

Further to the above personal exertion rules, the ATO continues to restrict income splitting arrangements to include Personal Service Entities as well as individuals. The allocation of professional firm profits is a key focus of the guidelines. Professional firms include but are not limited to those providing services in the accounting, architectural, engineering, financial services, legal, medical and management consulting professions.

These guidelines are concerned with whether there is a risk that professional profits are not appropriately taxed to the individual professional practitioner or where particular arrangements lack a commercial rationale and/or exhibit certain “high risk” features.

If your industry is affected by the guidelines, you should consider where you may stand and whether this aligns with the level of audit risk that you are willing to accept. Alternatively, changes to your structure or further decisions may be required to change your risk profile.

It is recommended to understand your professional profits allocation and assess your risk level in line with ATO guidance prior to 30 June to allow you to take any relevant action/s.

Personal loans from companies

If you are a shareholder or associate of a private company and have been provided by the company money, value or financial benefits or used company assets for private purposes (without market-rate compensation), you may have unwittingly created a Division 7A loan with the company or a deemed dividend to the shareholder or associate. Ensure you review any transactions between the company and its shareholders and/or associates to understand any tax implications.

Any new loans created during the current year will be required to be repaid or put on a complying loan agreement before the earlier of:

- the date the company lodges its 2026 tax return; or

- the lodgement due date of the company’s 2026 tax return.

To avoid creating new Division 7A loans, it is essential you have made any necessary minimum loan repayments before 30 June 2026 to ensure no adverse tax consequences arise.

The interest rate for the Division 7A loans is 8.37% for the 2026 financial year.

Dividend payments – 45 day rule

Another area under the ATO’s microscope is the “45 day rule” (also called the holding period rule). Where taxpayers receive a franked dividend without holding shares “at risk” for at least 45 days (not counting the day you buy or sell them), they are not entitled to claim any franking credit tax offsets.

This issue is commonly encountered where a family trust makes franked dividend distributions to a corporate beneficiary that was incorporated after the original dividend ex-date. In such cases, the ATO may consider that the corporate beneficiary has not held shares at risk for the required 45 days, disallowing any franking tax credits from being claimed. This risk should be considered and understood where newly established entities are receiving franked dividend distributions.

To avoid the effective “double-tax” that arises from disallowed franking credits, we recommend reviewing your structuring early to ensure any planning does not fall foul of the 45-day rule.

The instant asset write-off is here to stay

Under the instant asset write-off (IAWO), small business entities (SBEs) with an aggregated turnover of less than $10 million can claim an immediate deduction for the business use portion of new depreciating assets acquired and improvements to existing assets which cost less than $20,000 (for the 2026 financial year).

Although temporary increases to the threshold have been legislated in recent years (particularly the post-COVID years), the permanent IAWO threshold has remained at $1,000. From 1 July 2026, the Government has proposed to make a permanent change in the legislation to keep the IAWO incentive for businesses at $20,000. This has not yet been made law.

Fringe benefits tax

Fringe benefits tax (FBT) broadly applies to non-cash benefits provided to an employee unless an exemption applies. The commonly applied exemptions include (but are not limited to):

- minor and infrequent benefits provided for less than $300;

- private use of a panel van, ute or other commercial vehicle (broadly being, one not designed principally to carry passengers where the private use is limited);

- the provision of portable electronic devices mainly for use in the employee’s employment;

- private use of an eligible electric car.

Where employers are providing non-cash benefits to employees that are exempt from FBT and not lodging FBT returns, we recommend lodging an FBT return annually to limit the amendment period.

Another focus area for the ATO in relation to FBT is on third-party or arranger provisions, where an employer facilitates a benefit provided by a third party to employees. The arranger provisions broadens the FBT scope to include benefits that employers may not even be aware of. Scenarios may include the following:

- Discounted membership prices with a gym (the third party).

- Free tickets to a sports game provided by the sports club, as a result of the club’s business relationship with the employer.

- A director of a company paying for staff meals with personal funds. In this case, the ATO views the director as an agent of the company. Therefore, the director is seen as a third party who provided a benefit as a result of the employment relationship.

Ensure you understand the benefits being provided to your employees or their family (or other associates) and whether any FBT is payable.

The ATO has the right to audit and amend FBT relating to prior years, for a period of up to six years from the date of an FBT assessment. If an entity has never lodged an FBT return, and therefore never received an assessment, the ATO can audit the entity for an unlimited number of prior years. This exposure can be limited by lodging an FBT return for the year ended 31 March 2026, thereby generating an FBT assessment.

Trust distributions

Discretionary trusts (and some fixed trusts) are required to prepare and execute distribution minutes prior to 30 June for each financial year. These distribution minutes detail how the income of the trust will be distributed to beneficiaries for the relevant financial year. Minutes must be prepared in accordance with the trust deed and detail any use of income streaming. For the 2026 financial year distribution minutes to be effective, they must be prepared and executed by 30 June 2026.

When preparing the trust distribution minutes, it is recommended to prepare the minutes in a way to retain a nominal amount in the trust for the 30 June 2026 income year. This will assist with generating a notice of assessment for the trust and effectively limiting the amendment period to 4 years.

Broadly, the amendment period is a particular tax period that the ATO or taxpayer are able to review and amend tax forms to include any under or overpayment of tax. The period is determined from the date of relevant notices of assessments. Where there is no retention of income, trusts are generally not taxable and therefore do not receive notices of assessment. As such, without completing the distribution minutes and retaining a nominal amount in the trust by 30 June 2026, the amendment period may be greater than 4 years.

Bad debts

Bad debts should be identified before 30 June 2026 to understand the commercial and tax implications. Therefore, a review of trade debtors should be conducted to identify any amounts that are considered uncollectable and these should be written off prior to 30 June 2026.

Broadly, where a bad debt is written off and been determined unlikely to be recovered through any reasonable and commercial attempts prior to 30 June 2026, you may claim a tax deduction for it in the 2026 financial year. This is on the basis that the debt is still in existence and has not been waived, forgiven, sold or extinguished in any other way.

However, the bad debt may not be deductible where there has been a change in ownership or control of a company or trust, unless the continuity of business tests are satisfied.

Year-end finalisation report

Employers should have procedures in place to ensure they are able to lodge the Single Touch Payroll (STP) year-end finalisation report by 14 July 2026. This will allow their employees to complete their tax returns.

Remember to include fringe benefits provided to employees in the STP finalisation report where the benefit provided is more than $2,000.

Prepayments

Broadly, businesses with an aggregated turnover below $50 million may deduct prepaid expenditure for the 2026 income year where:

- The total period covered by the prepaid expenditure is 12 months or less; and

- The period covered by the prepaid expenditure ends in the following income year (i.e. by 30 June 2027).

Businesses with an aggregated turnover below $50 million should review their expenses and, subject to cash availability, consider bringing forward any payments which are currently being paid monthly such as subscriptions and insurance.

In order to claim a deduction for this financial year, determine what expenses may be prepaid prior to 30 June 2026 using excess cash available.

Stock and depreciating assets

For tax purposes, most businesses that trade stock are required to do an annual stocktake as at 30 June. It is important to plan and execute a stocktake in a way which gives a reliable and accurate stock figure. As part of the stocktake, you should identify any old, obsolete or damaged stock which can be written off or written down.

The fixed asset register should also be reviewed to write off obsolete, scrapped or damaged depreciating assets before 30 June 2026.

Tax File Number reporting

Closely held trusts (including family trusts) are currently required to report the Tax File Number (TFN) and other personal details of any new beneficiaries. This is done by completing a TFN Report for the quarter the beneficiary quotes their TFN to the trust. The TFN report must be lodged by the end of the month following the relevant quarter. As such, any beneficiaries of a trust for the year ended 30 June 2026 that have not quoted their TFN should do so by 30 June 2026. This will ensure the trust is able to lodge the June 2026 quarter TFN report by 31 July 2026.

Broadly, where a beneficiary’s TFN has not been quoted, the trustee is required to withhold tax at the top marginal tax rate plus Medicare Levy from any payments or distributions made to them.

Fortunately, from 1 July 2026, the Government proposes to phase out this separate reporting and instead trusts will be required to report beneficiary TFNs as part of completing the trust’s income tax return.

Payroll tax – Queensland

Where a business has Australian taxable wages that exceeded $1.3 million for the 2026 financial year, the entity must lodge the Queensland annual payroll tax return by 21 July 2026. If the entity has overpaid tax for the year, the amount will be applied to other outstanding debts or refunded.

It is important to note that in Queensland, a business must register for payroll tax within seven days after the end of a month in which the Australian taxable wages exceed $25,000 a week. This is required even if the business expects the Australian total taxable wages for the financial year to be less than the $1.3 million threshold.

Employers should be wary of common omissions, including interstate payroll tax registrations and contractor arrangements. Employers should confirm if contractor arrangements meet a relevant payroll tax exemption. Further, as regulators increase reliance on data-matching tools, businesses should confirm payroll tax aligns with Workcover, income tax, and STP data.

Learn more

Much like a successful EOFY shop, planning and preparation is essential for your tax affairs. Get in touch with your Pilot advisor to stay informed of your tax obligations and strategies for success.

If you would like assistance with tax planning or have any questions, please contact Kylee Smith or your Pilot advisor on 07 3023 1300.