Effective 1 July 2026, the new Payday Super rules will come into force, effectively requiring employers to pay superannuation guarantee (SG) contributions at the same time they pay employees’ wages or salaries. This new framework replaces the existing quarterly system, under which employers had 28 days after the end of each quarter to make SG payments.

Under the new Payday Super regime, SG contributions must be paid and received by the employee’s nominated super fund within seven business days of payday (with only limited exceptions such as for new employees).

Currently, due to the processes used by various third party clearing houses and other intermediaries, contributions often take longer to reach super funds, issues that Digital Service Providers (DSPs) are currently working to address.

Key Payday Super changes employers need to know

From 1 July 2026, Ordinary Time Earnings (OTE) will be replaced by a new concept called Qualifying Earnings (QE) as the new base used to calculate the 12% SG. QE includes amounts currently classified as OTE, commission payments and salary-sacrificed superannuation contributions.

Individual contractors who are paid mainly for their labour will fall under the expanded definition of employee (as they do in the current quarterly SG system). Payments to these individuals are also included in the definition of QE.

Which employers are affected by Payday Super?

The Payday Super reforms will impact all employers to some degree. However, employers with a higher payroll frequency (e.g. weekly or fortnightly) will need to make more regular payments under the new rules and face a heavier burden.

Why the Payday Super Reform matters for employers and their employees

The new rules will require businesses to prepare and update their systems and practices before 1 July 2026, including:

- Moving from four large quarterly payments to more regular payments will require cash flow to be closely monitored.

- Payroll systems, clearing house providers and other DSPs may need to be updated or changed completely to meet the new requirements.

- Businesses currently using the Small Business Super Clearing House (SHSCH) will need to move to other (commercial) clearing house operators before 1 July 2026, due to the impending closure of the SBSCH by the Government.

- The Australian Taxation Office’s (ATO) increased visibility with Single Touch Payroll means late payments will more easily be flagged automatically, increasing the risk of an ATO audit or review.

Payday Super Compliance: What employers must do to prepare

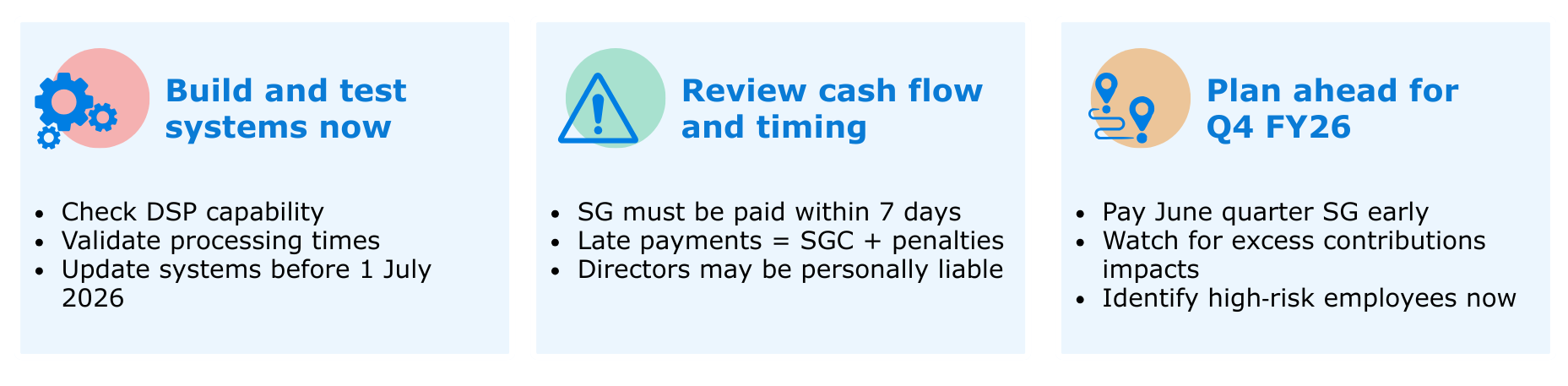

1. Build and test systems – now

One of the most pressing challenges for employers is ensuring payroll and payment systems can meet the seven-day timeframe. Given the final legislation was only passed on 4 November 2025, DSPs are still working on updates to support Payday Super and faster processing time frames.

Employers would be wise to focus their time to test and validate whether their current DSPs will meet the new requirements and attend to any required updates as soon as possible ahead of 1 July 2026.

2. Review Cash flow planning and payments timing

Under Payday Super, the timing of SG payments can materially affect employer cash flow given employers no longer have until 28 days after the end of each quarter to pay SG.

Late payments (even by one day) will trigger the superannuation guarantee charge (SGC), which includes a new notional earnings component (NEC) and potentially a range of administrative penalties on top of the original SG amount. This includes a 60% administrative uplift penalty if the employer does not lodge a voluntary disclosure statement before receiving an SGC assessment. Therefore, early detection and correction is critical to minimising exposures. Importantly, company directors can be made personally liable for SGC debts which remain unpaid.

The general interest charge (GIC) which applies on any outstanding amounts including SGC. GIC is not tax deductible.

3. Plan ahead for SG payments in the last quarter of FY 2026

Employers should be planning ahead to ensure that their SG contributions for the final quarter of the 2025–26 financial year (covering payments in the month of April to June 2026) are paid by the usual due date of 28 July 2026 (ideally earlier).

Where an employer pays the June 2026 quarter SG liability before 28 July 2026 (within the usual 28-day time frame) this may result in excess contributions for certain employees in the 2026–27 financial year. This may occur where the final June 2026 quarter and all 2026–27 financial year SG contributions are received in the 2026–27 financial year, resulting in total contributions above the concessional contributions cap (a $32,500 cap is expected to apply for the 2026–27 financial year, while a $30,000 cap applies for the 2025–26 financial year).

Having said that, at the time of writing this article, the Government is aware of this issue and has indicated it is considering introducing a transitional measure for the 2026–27 financial year where excess contributions arise from the “bunching” of SG contributions as explained above.

While we await further details regarding these transitional measures, we recommend employers review and identify high earning employees or those with existing salary sacrifice super contribution arrangements who are at higher risk of being affected by excess contributions.

Act now: Don’t delay preparations

To help reduce risks of non-compliance post 1 July 2026, we recommend planning and preparing for these changes as early as possible.

Employers may consider paying superannuation on payday now, and not wait until 1 July. This will allow sufficient time to upgrade and test new/updated systems before the start date, albeit with cash flow implications.

The top priority for employers is to seek confirmation from payroll providers and DSPs on their current processing time frames and what needs to be done to comply with the new rules. With time running short until the 1 July deadline, make sure your business isn’t left behind.

Contact Pilot

If you would like our assistance in reviewing your payroll systems or business planning ahead of the new regime, please contact Kylee Smith, Kristy Baxter or your Pilot Advisor on (07) 3023 1300.